Tax Policy – Comparing the Growth and Income-Boosting Effects of Tax Reform Options

As policymakers evaluate changes to the tax code, such as proposals coming from presidential candidates and the White House, it will be important for them to evaluate the relative effects of various provisions. There are many ways to raise a dollar of revenue, and many ways to offer tax relief—some tax changes are more efficient than others, providing more economic benefit for less change in revenue. In other words, policymakers ought to be asking, “How can I get the most bang for my buck?”

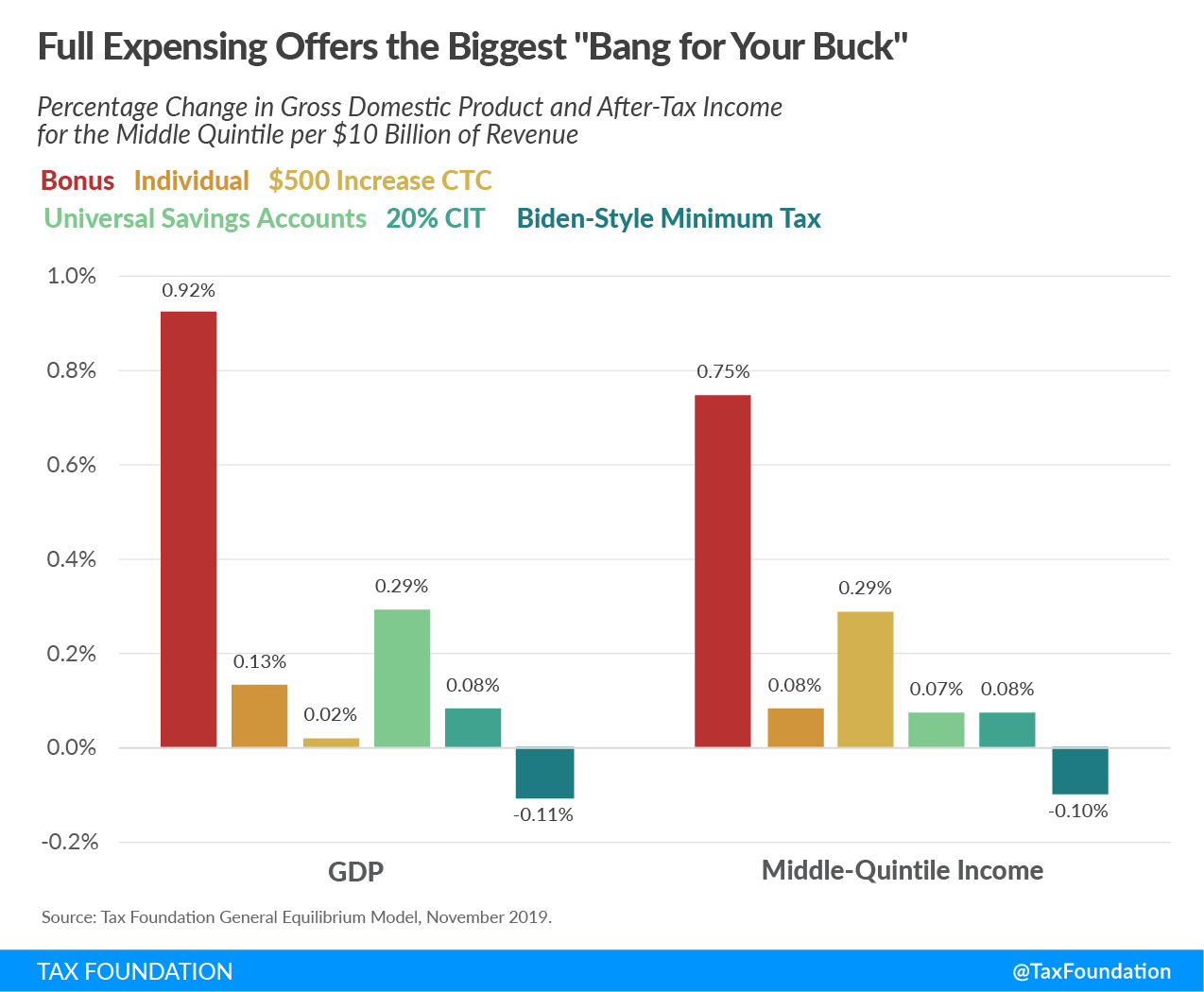

We’ve used the Tax Foundation General Equilibrium Model to compare four tax reductions and one tax increase: making Tax Cuts and Jobs Act (TCJA) 100 percent bonus depreciation permanent, making the TCJA individual provisions permanent, increasing the child tax credit (CTC) by $500, implementing a $10,000 Roth-style universal savings accounts (USAs) for taxpayers making under $200,000, and implementing a corporate minimum tax such as one proposed by former Vice President Joe Biden.

The chart below shows the estimated change in gross domestic product (GDP) and after-tax income for taxpayers in the middle quintile (40 percent to 60 percent) per billion dollars of revenue for each policy

Once made permanent, 100 percent bonus depreciation would generate more long-run economic output and a larger increase in after-tax income per dollar of forgone revenue than the other four proposals. Making bonus depreciation permanent would be one of the most efficient ways to increase after-tax incomes for the middle class.

Comparisons like this can help improve the process of navigating upcoming TCJA expirations and staking out new policy ideas. For example, we estimate that making the individual provisions permanent would increase long-run economic output by 2.2 percent, but this would reduce long-run federal revenue by $165 billion annually. On the other hand, permanence for TCJA 100 percent bonus depreciation would increase economic output by 0.9 percent at a long-run annual cost of $10 billion of revenue. Proposals such as USAs, a larger child tax credit, or a 1 percentage point corporate rate reduction are less efficient tax cuts in terms of economic output, while a corporate minimum tax is a less efficient revenue increase. See the tables below for the macroeconomic and distributional effects of all five policies.

Keeping in mind which policies offer the most cost-effective growth helps illustrate the economic and distributional trade-offs among different tax proposals.

|

Source: Tax Foundation General Equilibrium Model, November 2019. |

|||||||

| Proposal | 100 Percent Bonus Depreciation Permanent | TCJA Individual Provisions Permanent | Universal Savings Accounts | Maximum Child Tax Credit Increase to $2,500 | Reduce Corporate Income Tax to 20 Percent | Corporate Minimum Tax | |

|---|---|---|---|---|---|---|---|

| Gross Domestic Product | 0.9% | 2.2% | 0.04% | 0.06% | 0.1% | -0.3% | |

| Capital Stock | 2.2% | N/A | 0.07% | 0.1% | 0.1% | -0.7% | |

| Wages | 0.8% | 0.9% | 0.01% | 0.03% | 0.1% | -0.2% | |

| Full-Time Equivalent Jobs | 172,000 | 1.5 million | 6,750 | 88,000 | 23,000 | -56,000 | |

| Conventional Long-Run Annual Revenue (billions) | -$10 billion | -$165 | -$1.4 | -$29 | -$12 | $26.6 | |

|

Source: Tax Foundation General Equilibrium Model, November 2019. |

||||||

| Income Group | 100 Percent Bonus Depreciation Permanent | TCJA Individual Provisions Permanent | Universal Savings Accounts | Maximum Child Tax Credit Increase to $2,500 | Reduce Corporate Income Tax to 20 Percent | Corporate Minimum Tax |

|---|---|---|---|---|---|---|

| 0% to 20% | 0.76% | 1.2% | 0% | 0.36% | 0.1% | -0.32% |

| 20% to 40% | 0.73% | 1.6% | 0% | 1.26% | 0.09% | -0.25% |

| 40% to 60% | 0.73% | 1.4% | 0.01% | 0.84% | 0.09% | -0.26% |

| 60% to 80% | 0.70% | 1.6% | 0.01% | 0.48% | 0.09% | -0.25% |

| 80% to 100% | 0.79% | 1.5% | 0.02% | 0.06% | 0.09% | -0.40% |

Source: Tax Policy – Comparing the Growth and Income-Boosting Effects of Tax Reform Options

Upstate Tax Professionals

Upstate Tax Professionals